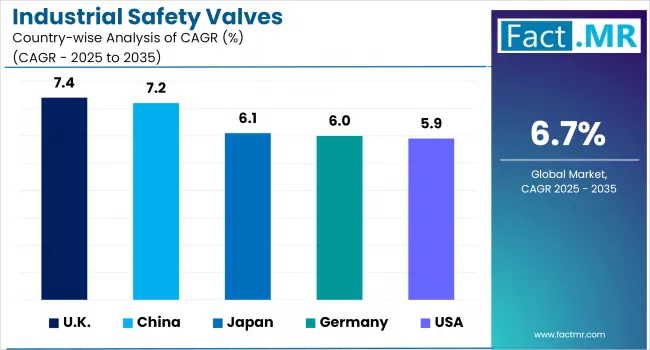

According to a market summary of a report by research and consulting firm, Fact.MR, the global industrial safety valve market is expected to reach more than USD $10 million by 2035, an increase compared to over USD $5 million in 2024. During the forecast period from 2025 to 2035, the industry is projected to expand at a CAGR of 6.7%.

Text & images from Fact.MR

Industrial safety valves play a critical role in maintaining operational safety in oil & gas, chemical, power generation, and manufacturing industries by preventing overpressure conditions and equipment failure. These valves support regulatory compliance, equipment protection, and worker safety. With advancements in automation, smart valve technologies, and predictive maintenance, they offer improved efficiency and reliability in hazardous applications.

What are the Drivers of the Industrial Safety Valve Market?

The industrial safety valve market is supported by rapid industrialization and adherence to safety standards across sectors such as oil & gas, chemical processing, power generation, and pharmaceuticals. Increased attention to workplace safety — shaped by government regulations and industry frameworks such as OSHA, API, and ASME — is prompting manufacturing plants and industrial facilities to expand

the use of safety valves.

Another key factor is the expansion of process industries that require stringent safety measures. Safety valves are essential in preventing overpressure incidents involving pressure vessels, boilers, and pipelines, making them indispensable in sectors handling hazardous materials. As industrial systems grow more complex, the need for reliable safety mechanisms becomes more pronounced.

Technological advancement, including the adoption of smart valves for real-time monitoring, is also influencing the market. Applications of Internet of Things and Industry 4.0 technologies in safety valves, such as predictive maintenance, remote monitoring, and automation, help reduce operational risk and enhance process efficiency.

Investment in oil and gas infrastructure — especially in emerging economies — continues to support safety valve demand. Rising refining capacity and the replacement of aging equipment across industries further reinforce market growth. Similarly, the energy sector, including nuclear and renewable power, is incorporating industrial safety valves to manage system pressure and reduce operational hazards.

Environmental protection concerns and the need to prevent leaks and emissions in chemical plants and refineries are also encouraging the use of high-integrity safety valves that meet elevated emission and safety standards.

The Regional Trends of the Industrial Safety Valve Market

The industrial safety valve market is led by North America, supported by its established industrial base, stringent regulatory frameworks, and increased infrastructure development spending. The region promotes the adoption of smart safety valve technologies in sectors such as power generation, oil & gas, and water treatment, particularly in the United States. The presence of leading manufacturers and adherence to API and OSHA standards continue to support market expansion.

Europe follows closely, with countries such as Germany, France, and the U.K. prioritizing industrial safety in accordance with stringent EU safety regulations.

Adoption of smart safety valve systems is supported by the region’s focus on renewable energy, nuclear safeguards, and environmental protection. Germany, with its strong manufacturing base and integration of Industry 4.0 technologies, demonstrates significant use of smart safety valve solutions.

Asia-Pacific is undergoing consistent market growth, supported by accelerated industrialization, investment in energy sector infrastructure, and increasing safety awareness. India and China are key contributors, driven by demand in oil refining, chemical processing, and power generation.

Government initiatives and foreign investment in the manufacturing sector are further reinforcing growth. Japan and South Korea also represent important regional markets, characterized by advanced production capabilities and well-regulated industrial systems. The Middle East and Africa are developing gradually, driven by oil & gas exploration, particularly in the Gulf Region.

Construction of new petrochemical and refinery facilities is contributing to the safety valve demand. However, economic uncertainty and fluctuations in crude oil prices may influence investment in safety-related products. In Latin America, with Argentina and Brazil as leading contributors, industrial development and government efforts to improve workplace safety are shaping market demand. Growth in the energy and mining sectors is expanding the use of industrial safety valves. Challenges persist with uneven regulatory compliance and broader economic instability, which may limit progress in some areas.

The Challenges and Restraining Factors of the Industrial Safety Valve Market

Even though the growth trajectory remains steady, there are several obstacles that may challenge the industrial safety valves market in the near term. One of the primary constraints is the high cost of next-generation safety valve technologies. Intelligent and autonomous safety valves equipped with predictive maintenance and real-time monitoring capabilities are capital-intensive when considered alongside infrastructure investment and software integration.

This may make them less accessible for mid-sized and small-scale operators. Compliance and certification requirements present another challenge. Regulatory approvals for industrial safety valves are time consuming and expensive, as products must meet multiple international standards including ASME, API, and ISO. The complexity of certification procedures across different regions creates barriers to market entry and product launch timelines. They also add to operational costs. Maintenance costs and operational inefficiencies are also limiting factors.

stringent EU safety regulations, which contributes to the growth.

As pressure-handling devices, safety valves require regular maintenance to ensure consistent functionality. Malfunctions or breakdowns can lead to costly downtime and safety risks. Maintenance and replacement needs contribute to total cost of ownership, which may discourage upgrades in price-sensitive segments. Moreover, supply chain instability and raw material price volatility impact production costs. Price-sensitive materials such as stainless steel, industrial alloys, and elastomers used in the manufacturing of advanced safety valves are subject to fluctuation. Global shortages of semiconductors have also disrupted the production of smart safety valves, leading to shipment delays and increased costs.

Despite these challenges, the medium-term outlook for the industrial safety valve market remains positive. Increased investment in automation, strengthened safety regulations, and broader implementation of Industry 4.0 technologies are expected to support market development. Advances in materials science, sensor integration, and AI-driven predictive maintenance are expected to enhance reliability and performance, supporting continued business expansion.

Country-Wise Outlook: The U.S. Safety Valve Market Expands Amid Automation and Environmental Compliance

The U.S. industrial safety valve market is growing incrementally. This is owed to heightened industrial safety regulations, growth in manufacturing activities, and growing industrial applications of automation. The OSHA and EPA stringent safety and environmental regulation compel industries to use high-performance safety valves.

The industry is also complemented with huge investment in infrastructure like oil & gas, chemicals, and power generation sectors, where the safety valves are one of the key drivers of operational reliability. Industry 4.0 technologies with IoT monitoring are driving further market growth. Industrial automation, valve joint ventures, and advanced innovations are also causing market competition.

For further reading or to purchase the report visit www.factmr.com